Have you been curious about P2P lending? And yet weren’t sure where to begin, you’re in the right place. This guide breaks down everything you need to know about manually lending money to borrowers. From lending money for the first time to how it comes back as repayments.

What’s Manual Lending All About?

It means you’re in the driver’s seat. You pick which borrowers get your money based on whatever criteria matter to you. Be it the duration, risk level, interest rates, or their income.

This works well if you like having control over your lending portfolio and want to build something that matches your comfort zone with risk.

Here’s How It Works

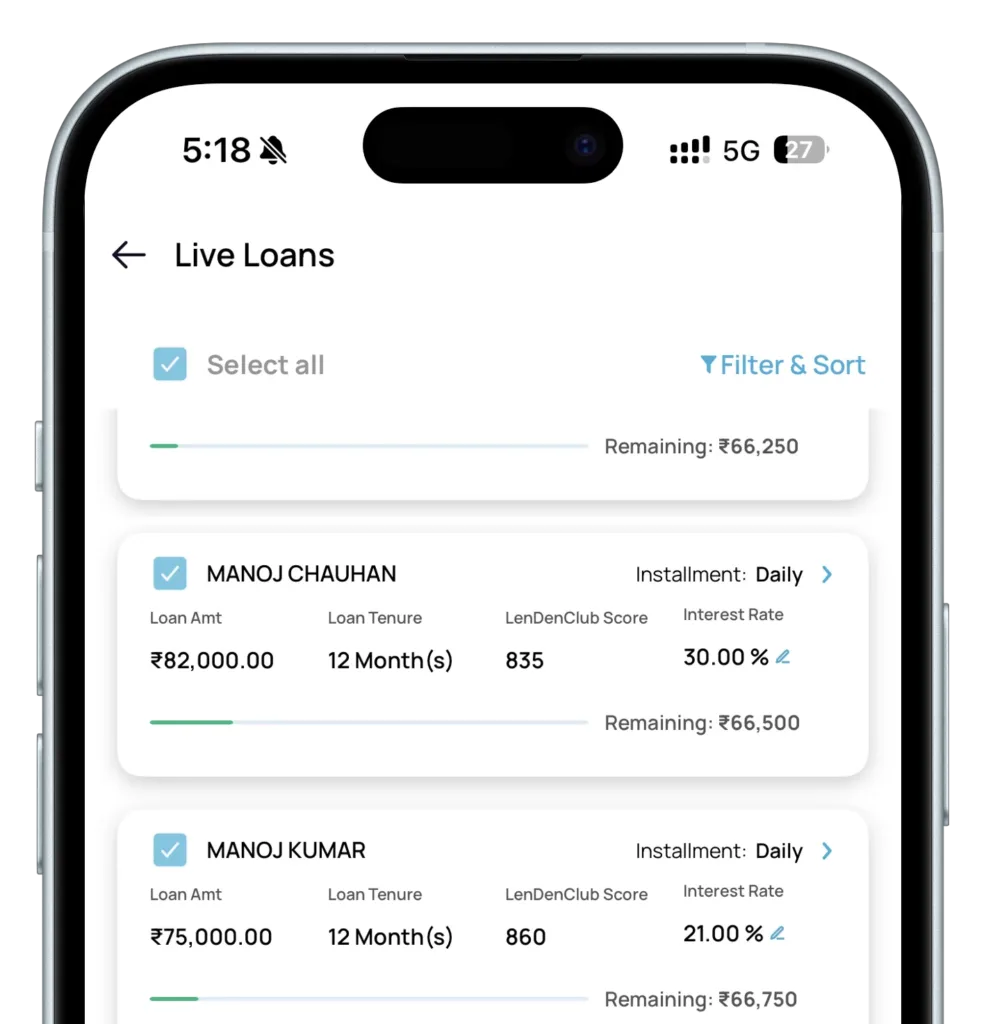

Step 1: Head to Dashboard

Open your LenDenClub dashboard and tap on “Live Options” or Manual Lending from the bottom menu. What you’ll see is a list of lending requests that have already cleared the approval process. These borrowers have been verified and assessed. Every listing shows you borrower details so you can make decisions with your eyes open. These borrowers have been through KYC checks, credit assessments, income verification and more.

Step 2: Filter Your Options As Per Your Need

You can narrow down your choices using several filters & sorting options:

Duration: Pick borrowers from 2 month to 12 months

Payment style: Monthly EMIs or daily repayments

Risk level: Low, medium, or high

Borrower income: Stick to certain income brackets if you want

Borrowing Amount: Filter by the amount being borrowed

You can also sort everything by LenDenClub Score, interest rates, or other factors. Basically, you’re building your own lending criteria here.

Step 3: Pick Your Borrowers

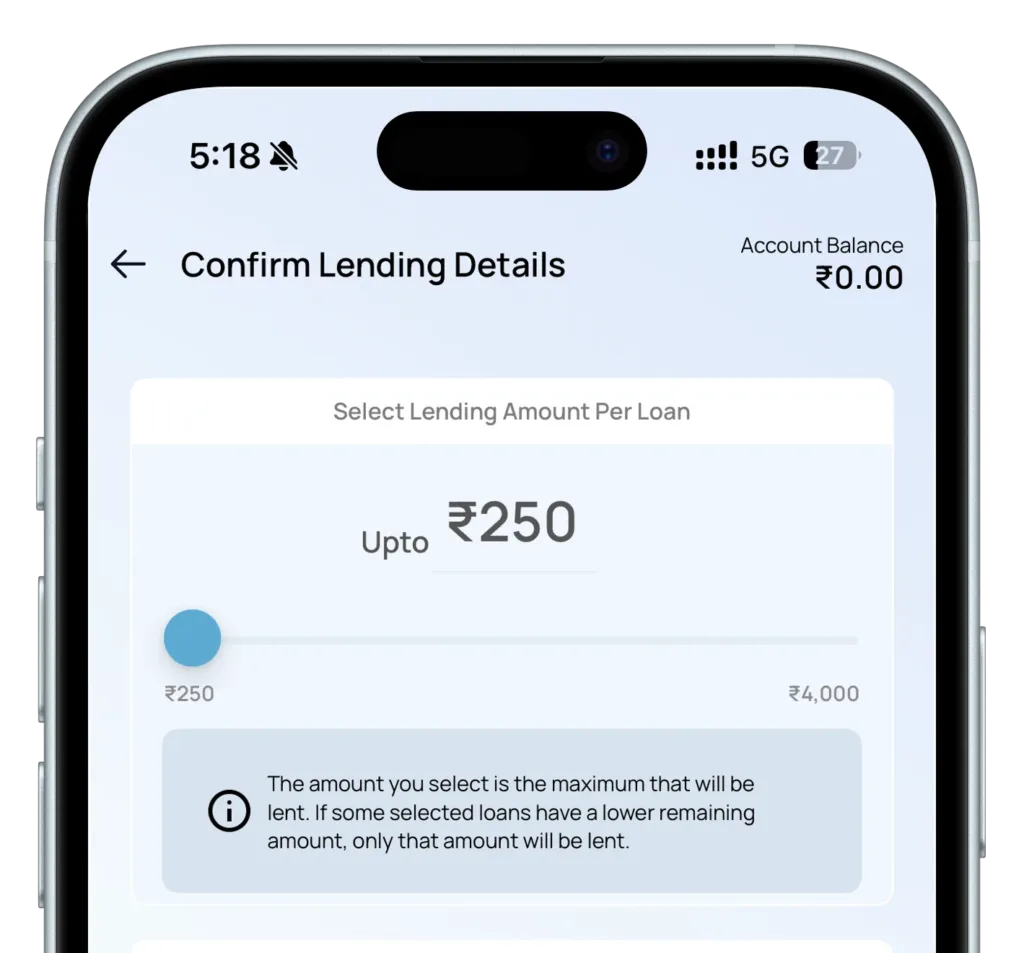

You can select up to 150 borrowers at once. There’s even a “Select All” button to speed things up.

Why so many? Because you don’t want to put all your eggs in one basket. If you spread ₹25,000 across 100 different borrowers at ₹250 each, and if one borrower defaults it only cost you ₹250. But if you’d put that entire amount into one borrower, you’d lose everything if they don’t pay back.

Step 4: Choose Your Amount Per Borrower

Now decide how much goes into each borrower. The minimum is ₹250, which makes this accessible even if you’re testing the waters.

A solid starting point: if you’re choosing 100 borrowers, put in at least ₹25,000 total (₹250 per borrower). This gives you proper diversification.

All you have to do is adjust the amount based on how confident you feel about a specific borrower or how risky they seem.

Step 5: Pay and You’re Done

Time to fund your selections. Payment options include:

UPI for quick transactions

Net banking

Bank transfer (IMPS / NEFT / RTGS)

Once payment is cleared, your money goes to the borrowers you selected.

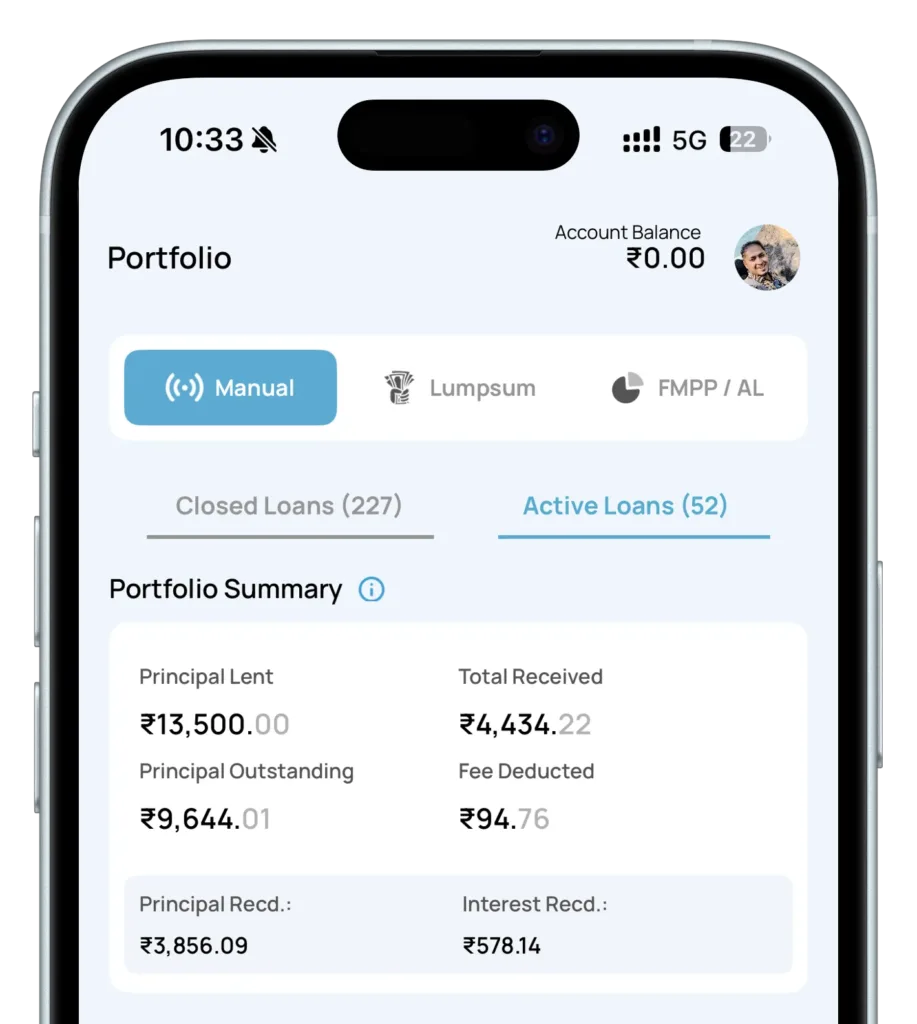

When Does Your Money Come Back?

After borrowers receive their funds, repayments start flowing back to you. These include your original amount (principal) and your earnings (interest) as and when paid by the borrower.

Timing depends on when the money was disbursed.

For monthly instalment/repayment (EMI) loans:

1st to 20th of the month The next month Lending amount disbursed on 2nd November → Repayments start 1st December

After the 20th of the month The month after next Lending amount disbursed on 21st November → Repayments start 1st January

Daily repayment / instalment loans (EDI):

These start almost immediately. Usually from the next day the lending amount is disbursed. Great if you want money coming back quickly or plan to relend soon.

Where Do You Receive Repayments?

According to the RBI regulation, everything goes straight to your bank account. Not to a wallet, not anywhere else—directly to your registered bank account.

LenDenClub is India’s largest peer to peer lending platform which started operations in India in 2015. We have been helping lenders diversify their portfolio beyond traditional investment instruments ever since.