Delaying Investments: A Great Way to Lose Tomorrow’s Money Today

Financial setbacks can happen to anyone, anytime. But they only catch you off guard if you’re unprepared.

Imagine someone who takes loans or cuts expenses when something unfortunate happens. They’re mostly just one big blow away from landing in a financial abyss. Now compare that to someone who invests proactively and builds an emergency fund. They not only get out of the situation at hand, but they also recover from it way quicker. That’s the power of mindful investment.

So, if you’re someone who tends to delay investments, this blog is for you. Read on to find out how it’s actually costing you more than you realise.

Understanding the Cost of Delay

As Indians, we’re naturally risk-averse. Despite growing awareness, SEBI’s Investor Survey found that only 9.5% of households in India actively invest in securities market products. But have you wondered what it is costing you? Consider this example:

Suppose you’re 35 years old, aiming to retire by the age of 60. You have 25 years to build the corpus you need to live comfortably after retirement. Let’s suppose the amount is ₹1 crore.

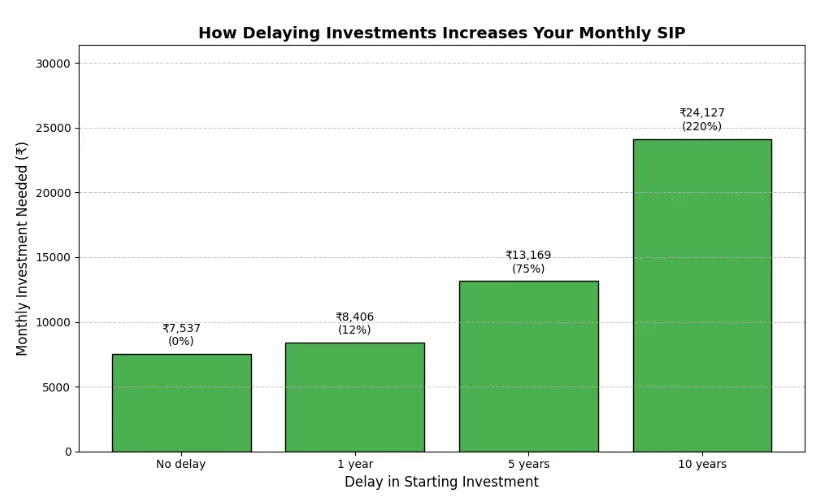

Assuming 10% average annual returns compounded monthly, if you start investing immediately, you will need to invest approximately ₹7,537 per month to reach your goal. This might sound like a hefty amount, but wait till you see how it inflates while you “wait”.

| Delay | Years to Invest | Monthly Investment Needed | Extra Per Month | Extra Per Year |

| No delay | 25 years | ₹7,537 | – | – |

| 1 year | 24 years | ₹8,406 | ₹869 | ₹10,428 |

| 5 years | 20 years | ₹13,169 | ₹5,632 | ₹67,584 |

| 10 years | 15 years | ₹24,127 | ₹16,590 | ₹199,080 |

In a nutshell, holding off on investments:

- For 1 year, increases your monthly investment burden by ≈ 12%

- For 5 years, increases your monthly investment burden by ≈ 75%

- For 10 years, increases your monthly investment burden by ≈ 220%

Because of compounding, time does most of the heavy lifting. But when you start late, you lose compounding years. Hence, to compensate, you must contribute more money every month.

But that’s not all. The deeper impact is opportunity cost.

During those first 10 “delayed” years, ₹7,537 invested monthly would have compounded to approximately ₹15.4 lakhs (₹7,537/month for 120 months, compounded monthly at 10% p.a.). This growth opportunity is lost permanently, alongside the permanently higher monthly contributions you’ll need to make.

Why Invest Early?

If you’re still on the fence about why you should start investing as early as possible, here are a few reasons to consider:

1. The Compounding Effect

The longer you leave your money invested, the more your returns grow on top of your previous returns, making your wealth grow faster over time. This is called the compounding effect, and it’s arguably the best advantage of investing early.

2. Higher Risk Tolerance

The earlier you start, the more risk you can afford to take. With a longer horizon, you can invest more aggressively in equity or growth-oriented instruments, knowing you have years to recover if markets dip.

3. Better Volatility Recovery

Market fluctuates—there’s no avoiding that. But when you start early, a market dip isn’t a setback; it’s a buying opportunity. More time means you can ride out downturns, average your costs over time, and recover losses well before you actually need the money.

4. Improved Financial Habits

Investing early instils discipline. When a portion of your income is committed to investments every month, you naturally spend more mindfully, plan better, and build a healthier relationship with money over time.

5. Less Financial Pressure

Starting early means you need to invest smaller amounts to reach the same goal. As the table above shows, a 10-year delay can triple your required monthly contribution. The earlier you start, the lighter the burden, leaving more room for life’s other financial priorities.

| Pro Tip: Start with whatever you can, even ₹500 a month. As your income grows, increase your contributions accordingly. Small, consistent investments started early will always outperform large, rushed ones started late. |

Exploring Alternative Investments: P2P Lending

Once you’ve built the habit of investing early, the next natural step is to optimise your portfolio for better returns. For salaried professionals and business owners already invested in mutual funds or FDs, Peer-to-Peer (P2P) lending offers a structured way to diversify into fixed-income alternatives with potentially higher yields.

P2P lending connects lenders directly to borrowers through RBI-regulated platforms like LenDenClub, bypassing traditional banking intermediaries. For investors seeking predictable debt-based returns to complement their equity exposure, it can serve as a meaningful portfolio addition.

That said, it warrants careful allocation. Following RBI’s revised guidelines in August 2024, platforms can no longer offer credit guarantees or assured returns, and lenders bear the full risk of principal and interest loss in the event of borrower defaults. The recommended approach is to limit P2P exposure to a small portion of your overall portfolio and diversify across multiple borrowers to manage concentration risk.

Used thoughtfully, P2P lending may enhance a portfolio’s yield profile, but it also introduces borrower default risk and potential capital loss. Therefore, it should be allocated conservatively and treated as a higher-risk fixed-income component within a diversified investment plan.

Note: P2P lending is not a guaranteed return product. Allocate carefully, diversify across borrowers, and use it as one component of a broader, well-structured investment plan.

Disclaimer: P2P lending is subject to risks. And lending decisions taken by a lender on the basis of this information are at the discretion of the lender, and LenDenClub does not guarantee that the loan amount will be recovered from the borrower.

The Early Bird Gets the Worm: Start Your Investment Today

The math is clear. Every year you delay costs you more than the year before. Whether it’s the higher monthly contributions, the lost compounding, or the opportunity cost of years left idle, waiting is never the neutral choice it feels like. The best time to start was yesterday. The second-best time is today.

You don’t need a perfect plan or a large sum. You just need to start.

If you’re ready to take the next step and explore how to make your money work harder, LenDenClub’s resources can help you understand your options, from building a diversified portfolio to exploring alternative investments like P2P lending.

Frequently Asked Questions (FAQs)

Delays reduce the time your investments have to compound, meaning you’ll need to invest significantly more later to reach the same goal.

Holding cash for emergencies is wise, but keeping excess funds idle leads to lost growth opportunities and doesn’t beat inflation.

Compounding is when your returns start earning returns themselves. The longer your money is invested, the more powerful compounding becomes.

The money you could have invested and compounded during the delay period is permanently lost, increasing the burden of future contributions.

Early investing allows you to take more calculated risks because you have time to recover from short-term market fluctuations.

Team LenDenClub

LenDenClub is India’s largest peer to peer lending platform which started operations in India in 2015. We have been helping lenders diversify their portfolio beyond traditional investment instruments ever since.