What is peer to peer lending?

As the name suggests, P2P lending (peer-to-peer lending) is a concept in which individuals or institutes can lend money to borrowers. The system removes the role of a financial institution as an intermediary. Instead, P2P lending platforms act as facilitators for the transaction of money.Anyone can

become an investor on P2P lending platforms and effectively lend to many individuals or businesses sitting at home. This mode of lending and borrowing has increased its adoption as an alternate way of financing.Peer to Peer lending started almost a decade ago, in 2012, with very few players. The industry is expected to grow at a rate of 21.6% CAGR to reach over USD 10 Billion by 2026.The Reserve Bank of India started to regulate this industry in India in 2017. The

master guidelines from RBI came into effect on 4th October 2017. Oversight from the country’s highest regulatory body has brought recognition and interest in the industry.

How does P2P lending work?

P2P lending websites source borrowers and investors on the platform. Both these parties are then directly connected. Each platform may have its own set of rates and terms, which both the investor and borrower needs to accept before making any transaction.

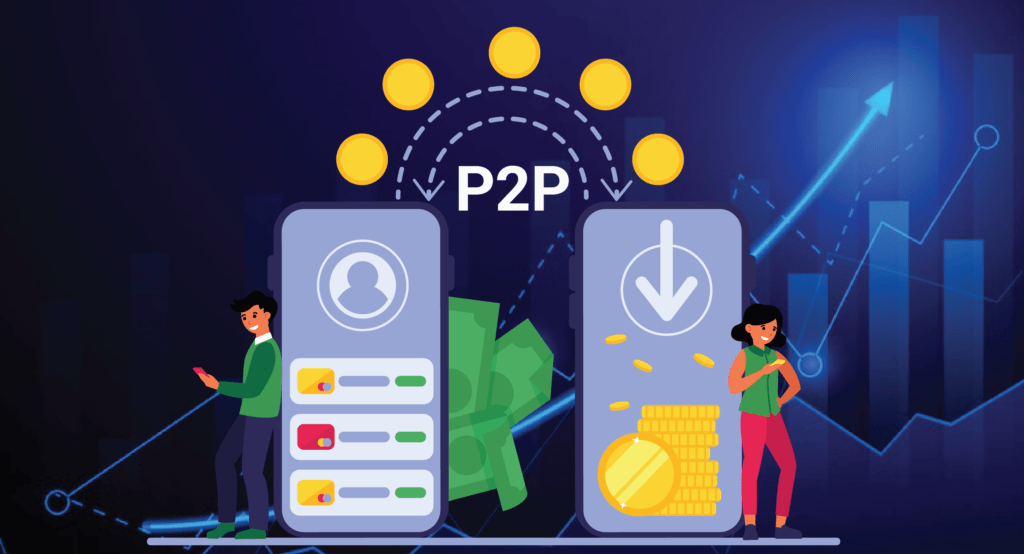

Illustration of a borrower and lender in the P2P lending platform

Firstly, a borrower can request a loan on the platform. The platform is responsible for completing the KYC of the borrower. They are also expected to complete

credit underwriting using various data points collected from the borrower. Once the due diligence is done, the borrower can accept the offered terms and accept. Once accepted the transaction is completed between both parties, which can be completely automated or manual.Platforms can decide the type of loans they want to offer, such as personal loans, business loans, invoice discounting, medical loans etc.

History of Peer to Peer lending in India

Peer to peer (P2P) lending in India is a relatively new concept, with the first P2P lending platform launching in 2012. However, it has seen rapid growth in recent years as more and more individuals have turned to P2P platforms as an alternative to traditional lending institutions.The Reserve Bank of India (RBI) issued guidelines for P2P lending platforms in 2017 and the sector got the legal recognition in 2018. The RBI has set up a regulatory framework for P2P lending platforms, including registration and compliance requirements and risk management and data protection guidelines.The P2P lending platforms in India are typically focused on providing small loans to individuals and small businesses, and they have been credited with helping to increase financial inclusion in the country. However, the industry has also faced challenges, such as concerns about fraud and defaults. Despite this, P2P lending in India continues to grow rapidly and is expected to become a significant source of alternative financing in the future.

Conclusion

P2P lending has both pros and cons. As an individual, you need to identify these and decide if this is the right instrument to fulfill your financial needs. Where investors can earn high returns, borrowers can get speedy loans. Do remember that P2P investments are subject to default risk. So before investing, ensure that you have researched and reviewed the

platform’s performance.