Are Provident Fund Savings Sufficient for Retirement?

Overview

A provident fund is a popular saving scheme in India. It offers many benefits, including high-interest rates and tax savings. However, whether it can help build a sufficient retirement fund depends on aspects like lifestyle, emergencies, and inflation.

Most of us spend our working years diligently contributing to the provident fund, with the promise of a secure retirement on the horizon. But as we inch closer to that golden phase of life, a question looms: Are provident fund savings truly sufficient to fund a secure, safe, and stress-free retirement?

In this comprehensive article, we will take you through certain factors of provident funds to assist you in making an informed decision.

Check out these Best investment plan in India for middle class

What is a Provident Fund?

EPF is one of the most popular and primary sources of retirement funds for Indian employees. Under this, employees and their employers contribute an equal amount (around 10-12% of the employee’s basic salary) to the EPF account. The collected amount can be used as a retirement fund by the employee.

EPF offers many benefits. The current interest rate on EPF is 8.15%, which is higher than other low-risk investment returns. It is also available for deductions under Section 80C of income tax.

Know: Retirement Planning in India, Strategies for a Comfortable Tomorrow

Factors of Provident Funds

All the points mentioned above make EPF not only an attractive option but also good enough for retirement. However, let us also consider these elements of EPF:

Debt Instrument

EPF is primarily a debt instrument as EPFO can only invest up to 15% of the annual incremental deposits in equities. This means most of the amount is invested into debt securities.

While debt securities are safe investments, they do not have the potential to provide enough returns to outpace inflation. Equities are considered one of the few investments that can provide returns to beat inflation in the long term.

Learn: How to Retire Early in Your 30s?

Maximum Contribution Amount

You can only contribute 15% of your basic salary to EPF. Based on your employer’s choice, their contribution can be limited to 12% of ₹15,000. This restricts your ability to actually build up a retirement fund in EPF.

Another essential aspect to consider is that 8.33% of your employer’s contribution goes towards employees’ pension scheme, which carries no interest rate.

Inflation vs. Interest Rate

EPF interest rates are higher than other secure investments. However, are they enough to surpass inflation? Assuming the long-term inflation rate to be 6%, the difference between the present EPF interest rate and the inflation rate is only 2.15%.

India’s retail inflation rate reached 7.44% in July 2023. Considering India’s actual inflation rate, which has been rising over the years, it is safe to say that EPF interest rates cannot beat inflation.

Explore: Best investment plan for monthly income

Lowering Interest Rate

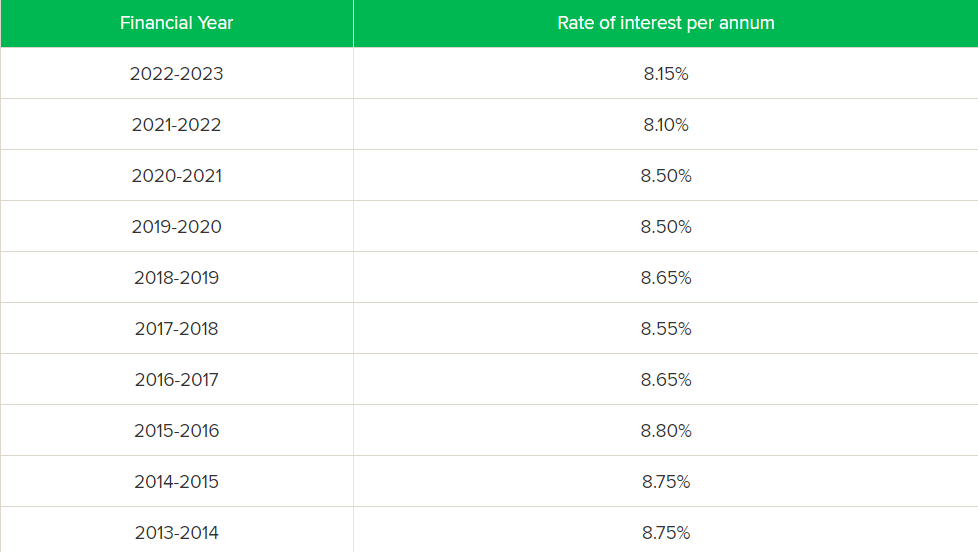

Over the past few years, the EPF interest rate has decreased. This table shows India’s EPF interest rates in the past decade.

In 2019-20 and 2020-21, the rate was 8.50%. It was brought down to 8.10% in 2021-22. While the rate did go up a bit this year (2022-23), i.e. 8.15%, it is not enough.

Is a Provident Fund Enough for Retirement?

Based on the features we’ve discussed, EPF can build up to a sizable amount over the years, provided there are no withdrawals. However, there is a fair possibility that it may not be enough to beat inflation.

Therefore, it is crucial to consider diversifying your investments and getting enough equity exposure. While investing in EPF, also consider investing in different options, such as:

- Public Provident Fund (PPF), Senior Citizens’ Savings Scheme (SCSS), and Fixed Deposits (FDs)

- National Pension Scheme (NPS)

- Mutual Funds and Systematic Investment Plans (SIPs)

- Equity

- P2P Lending

- Unit-Linked Insurance Plans (ULIPs)

To Sum Up

A provident fund is undoubtedly an attractive option to save for your retirement. However, it may be insufficient due to limitations like low returns, inability to outpace inflation, and a limit on contribution amount. Therefore, while saving for retirement, consider investing in other options like equities, SIPs, and NPS.

FAQs

1. What government schemes can I invest in for retirement savings?

You can invest in schemes like the Public Provident Fund (PPF), Senior Citizens’ Savings Scheme (SCSS), and National Pension Scheme (NPS). These are government-backed schemes that ensure stable returns.

2. How can I decide if my provident fund savings are enough for retirement?

You can calculate your estimated retirement expenses to decide whether your provident fund savings are enough for retirement. While doing this, also consider inflation and potential investment growth. You can then compare this amount with your estimated provident fund balance.

Team LenDenClub

LenDenClub is India’s largest alternate investment platform which started operations in India in 2015. We have been helping investors diversify their investments beyond traditional investment instruments ever since.